This article may contain affiliate links. I might earn a small commission if you make any purchases through my links and it comes at NO cost to you. For more information, please read my Disclaimer page.

If you are working toward being debt-free, you would agree with me that paying off your debt is one of the biggest financial blessings.

Paying off your debt buys you freedom. Freedom to do so many things in life, both personal and professional. For example, you can start saving and investing or work on building a business.

Once you are debt-free, the possibilities of achieving financial independence are endless.

But, first, you need to get to a place in life where you no longer have to worry about paying off your student loans or credit cards or any other form of debt you owe.

My philosophy on a mortgage is that a home is an asset, and you can classify that as an investment. Hence, it’s not technically debt (in my opinion).

To help and motivate you, I’ve put together the below steps you can take to pay off your debt.

So, let’s get into it right away.

1) Create An Action Plan

An action plan is a plan with steps you’ll be taking to achieve your goal(s).

You must create an action plan on how are you going to tackle your debt. I highly recommend not to wing it and make haphazard payments.

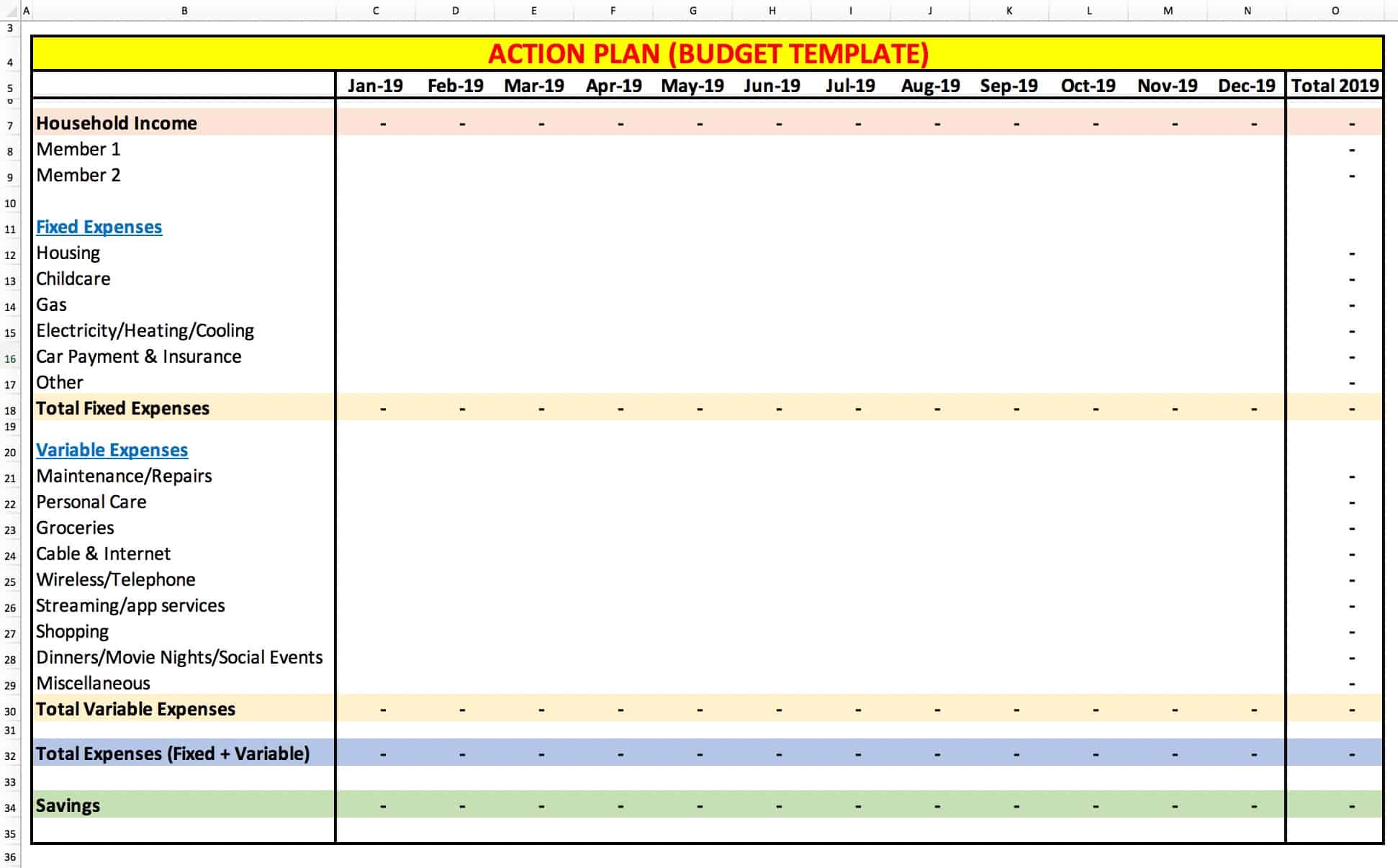

Create a detailed plan where you can identify all sources of your household income, list all monthly expenses, and ultimately determine your savings.

Here’s how you can approach this:

- Chalk out your income, expenses, and savings every month.

- Next, you want to layer in your debt from each account (student loans, credit cards, etc.)

- Determine if the amount you are saving is enough to cover the monthly debt payments.

- If yes, that’s great! If not, you’ll have to find innovative ways to either reduce your expenses or increase your sources of income.

A simple template like the one below should be good enough to put your numbers together.

Remember, the goal here is to determine how much you save every month.

Personal Note:

I used the above template religiously on a monthly basis to track my finances. It gave me peace of mind that I accounted for all my expenses and knew precisely at the end of the month, whether I saved or overspent.

The results were eye-opening.

Keep reading to find out how…

2) Determine If The Savings Will Be Sufficient To Offset Your Debt

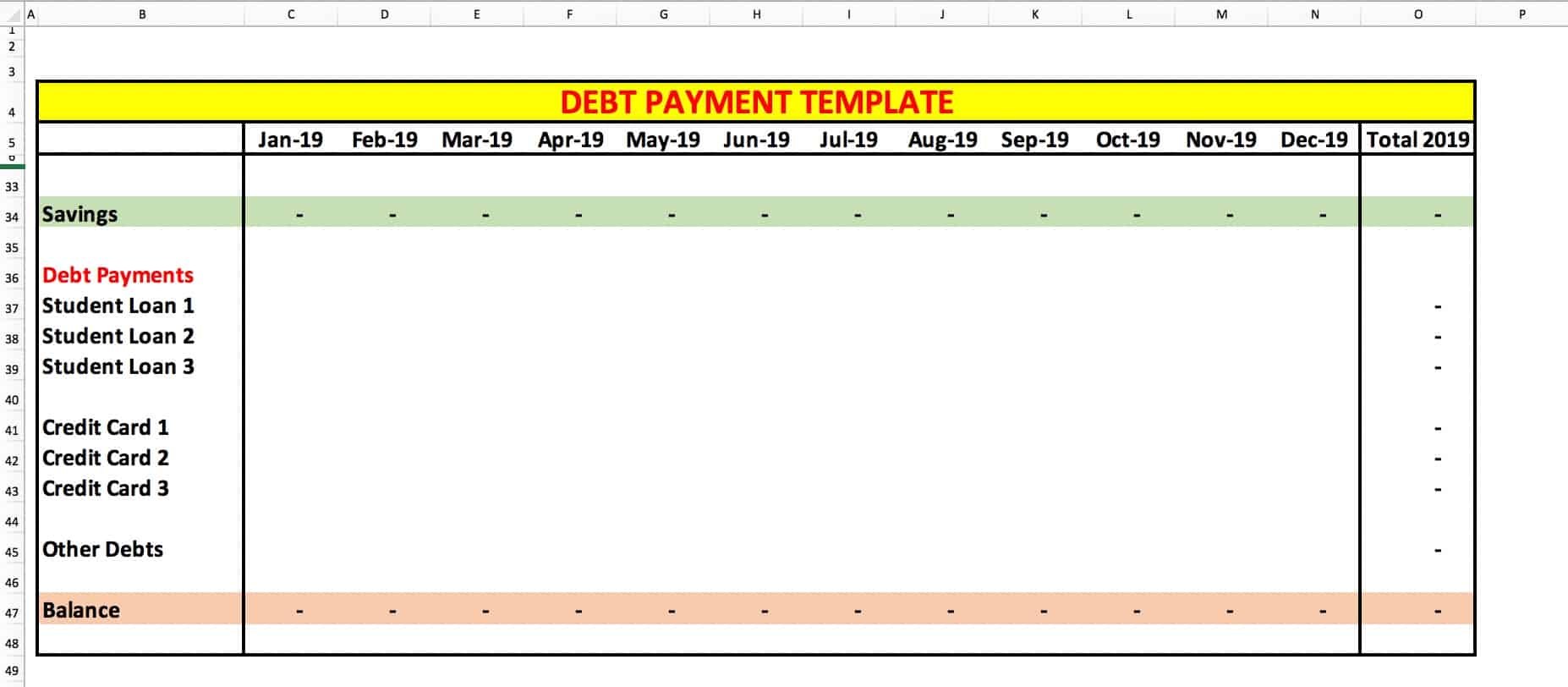

Once you have updated the details in the template shown in #1 above, you will have to layer in your debt payments.

I created a template below for you, so it’s easy to use and follow along.

As you can see from the image above, you can layer in the various debt payments you are responsible for paying.

The “Balance” line calculates how much debt can you offset. It will help you plan the next steps accordingly.

This is a critical step in the process as it will determine how you approach your payoff strategy. List every possible debt balance every month (even if it is $10/month) so you are laser-focused on your money.

When it comes to managing your finances, the results are a reflection of your plan of action, so I highly recommend to spend some time on this step and get it right.

It takes a while to get into a habit of tracking your finances consistently. If you want to pay off your debt quicker, make sure you are crystal clear in your approach.

Personal Note:

I started tracking my debts using the above template, and it was beneficial to see how I was performing. I am a numbers guy, so it was a little easier for me.

But, you don’t have to love numbers to pay off your debt. Just use the above format and focus on consistently updating and tracking your monthly finances.

I cannot emphasize enough how critical it is to be consistent with the process.

3) Earmark Your Money

This step will hold your entire strategy of paying off debt together. Here’s what I mean by that…

I’m going to assume that most of you have heard about Budgets. There is ample information, both good and bad on the internet about the budgeting process and budgets in general.

I have been in Corporate Finance, working with companies on their budgets, forecasts, strategic plans, and business partnerships for close to 15 years.

So, here’s my take on Budgets…

Most medium-sized companies and almost all big companies have yearly budgets.

Why?

Because budgets are a tool that you can use to both create a plan of action and use it as a guideline for your future.

The beauty of earmarking your money (you can also call it budgeting) is that you know exactly how much you planned to spend.

Consider yourself as a business entity that needs to plan for its finances, make income, pay for expenses, save, pay off your debt, and student loans and invest in its future.

It’s not any different from that.

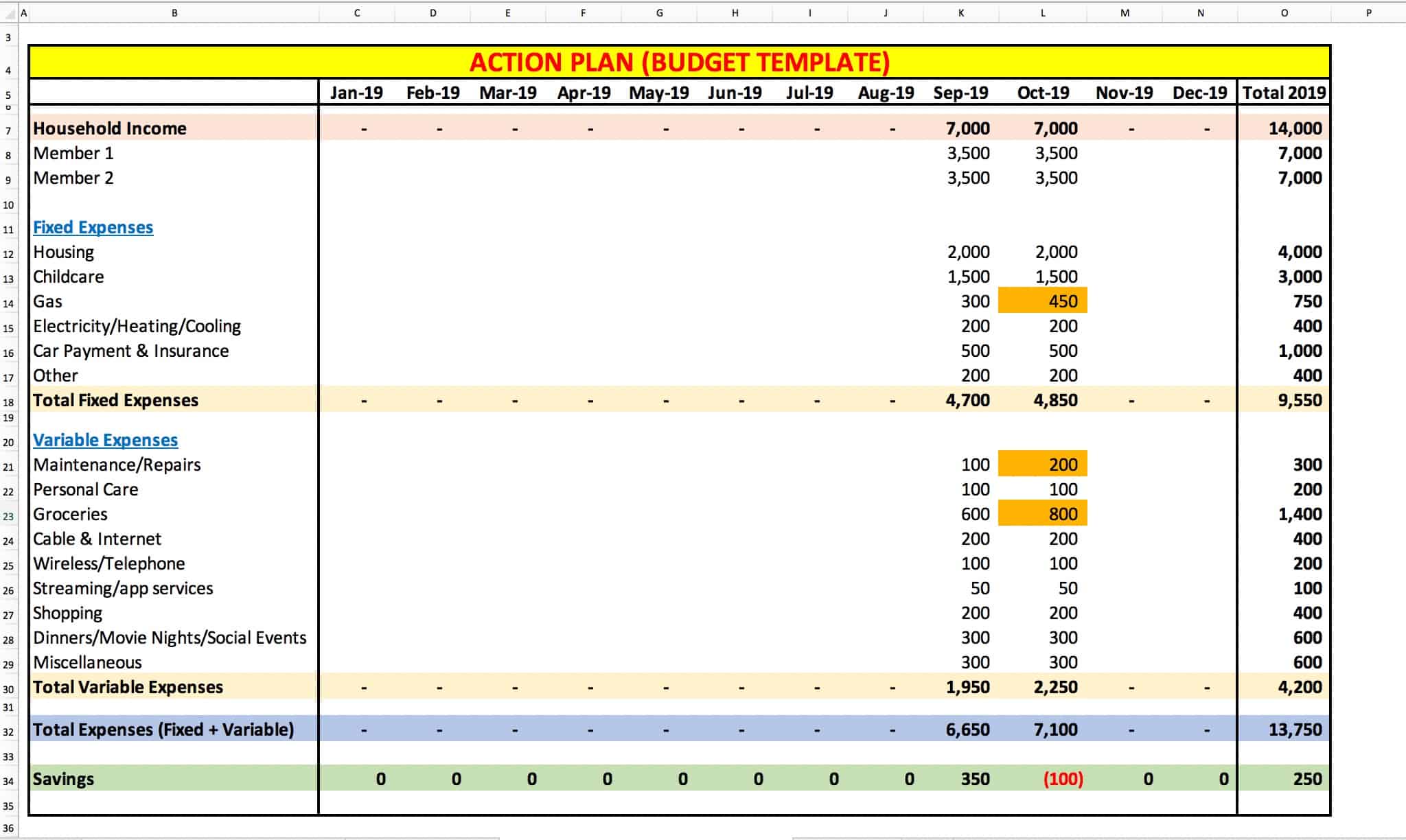

Based on your monthly income and expenses, earmark dollars against each of the categories in the Action Plan template (Step 1)

It might look something like this…

As you can see, you have your income, fixed expenses (one that you need to pay and can’t live without), and variable expenses (that you can make adjustments to) earmarked per month.

September – you plan to save $350

October – you are going to overspend by $100 (categories are highlighted in orange)

The above insight helps you take a proactive approach (especially for October) and figure out a way to save.

Personal Note:

The first couple of months were challenging for me and I did not have any savings 🙁 But, that meant that the process of tracking my money was working.

In the next couple of months, I had to dig deeper and make some adjustments in my lifestyle. I have to tell you that it was not easy and I hated it.

But, the motivation to be debt-free and pay off my student loans kept my drive alive!

4) Find Additional Income Sources

Continuing from #3, you know that in October, you are not going to save any money.

So, you have 2 options:

- Reduce your expenses for October OR

- Find additional sources of income

For option #1, try to adjust your spending in the variable expenses section first. If you can eat in one weekend or reschedule a movie night or shop less, it goes a long way in saving more.

If you have not yet checked out my article on how to save money, please do so. I talk about 25+ creative ways to save money.

So, if option #1 is not feasible, you have option #2. You’ll have to look for additional ways to bring in income.

You see my approach here?

No matter what, I want you to push yourself to save at the end of the month. This will help you pay off your debt faster and get one step closer to achieving your financial independence.

Personal Note:

I like investing in the stock markets and have been doing so for close to 13 years now. I wish I started earlier but barely had money to survive, let alone save and invest (here’s My Story)

My starting investment was minimal ($500), and I invested in stocks that could give me good returns. More importantly, I only invested in stocks that were considered SAFE investments vs. risky.

To learn more about the difference, please check out my article Safe vs. Risky Investments.

So, every month, I used to have a small amount of cushion from stock investments. In the event my expenses were higher than expected, I could tap into my buffer and re-route to pay off my debt.

There are hundreds of other options to save and bring in additional income:

- Take online surveys

- Drive people around on weekends

- Offer Dog walking services

- Use Ebates to earn cash back when you shop

- Offer Freelancing services (writing, designing, website creation, etc.)

You get the picture!

5) Use Cash For Your Purchases

I want to start with a caveat – if you think you are not good with credit cards, this is the option for you.

A lot of people use this as a go-to option for their everyday expenses. Some of my close family members and friends use cash and it works for them.

The idea is every week, you go to the bank/atm and withdraw a set amount of money. You use this for groceries, lunches, gas and other daily expenses.

The option to use cash prevents you from making unwanted purchases through your credit card. There are so many stories where people were able to cut down their expenses, save money and even pay off their debt by simply using this option.

There is certainly no harm in trying out this option if you haven’t already. If it helps to stay on track with your expenses, then you are in business.

Personal Note:

I use credit cards for almost all my purchases. The benefits are twofold (only if you are disciplined enough to pay off your monthly balance every month)

You see, if you do not pay your monthly balance and instead only pay the minimum amount due, you are charged interest on the remainder of the balance.

Most of the credit cards charge you close to 20% APR, which is insane. Here is the difference between interest rates and APR for credit cards, according to Experian.

If you want to pay off your debt quicker, accumulating credit card balances is counterproductive.

Almost all credit cards offer some benefit (cashback, reward points, miles, etc.) If you think about it, you can save additional money through these benefits.

You receive money into your account through cashback cards, redeem miles for your travel instead of paying for the ticket, and redeem your rewards points against most purchases you make daily.

You can both save money by taking advantage of the benefits and also use your savings to pay off your debt faster.

To me, that is a win-win situation and an excellent way to build your credit history.

6) Refinance Your Mortgage

One of the most common ways to pay off your debt quicker is to refinance your mortgage.

Mortgage payments are fixed expenses and a significant chunk of your monthly expense. If you can save 200 bucks a month by refinancing, that is huge (in my opinion)

To put things in perspective, the 200 bucks can cover your gas expense for the month or cover your monthly electricity/heating/cooling bill (in some cases it can cover both!)

You can use the refinance calculators available online to calculate your monthly savings. Here are a couple of options from QuickenLoans and BankOfAmerica.

Personal Note:

I refinanced my mortgage and saved close to $200/month on my mortgage payments. To me, that was a good chunk of money, and it covered my gas expense for the entire month.

Since your mortgage is long term, I would highly recommend this option as the amount you save over time is significant.

Also, you can use the savings from refinancing to pay off your debt.

7) Stretch Your Money

One of the many ways you can pay off your debt is to save money on everyday stuff through coupons and discount/promo codes.

You can subscribe (for free) to the rewards/loyalty programs and in turn receive discount coupons and special offers. The savings can add up significantly if you consistently follow this approach.

From groceries to gas stations to shopping for clothes or your home – this option can help you save a good chunk over time. You can use these savings to pay off your debt.

Personal Note:

I do all my groceries at Wegman’s and sometimes at BJs. Both of them have membership options and I end up receiving good deals.

BJs is a no-brainer since their gas prices are discounted by 15-20 cents. This not only helps cover the yearly membership costs but enables you to save.

For shopping, most of my wardrobe is from Kohl’s, and I am an MVC (most valuable customer), which means that every quarter, I receive coupons to avail 15% – 30% discounts on any purchases.

Sometimes at Kohl’s the savings end up in the range of $300 from a single visit.

Also, Amazon is now our go-to platform for household shopping. We are prime members which means, we get FREE shipping along with prime video and prime member deals.

Summary

To summarize, paying off your debt (including student loans and credit cards) not only requires an action plan but also requires the discipline from your end to follow through.

I used the above templates (shared in #1 and #2) every month to track my finances. I knew precisely how much I owed at the end of each month and year.

It was a little challenging initially (first 3-4 months), but once I made adjustments to my spending habits, I was able to save more and pay off my debt.

I was able to pay off close to $40,000 AND save 20% down payment (along with my wife), both within a span of 4 years with the above approach.

So, you have my permission to go ahead and be debt-free!

[convertkit form=908339]

Did you pay off your debt? Please share your experience with the different ways you used to become debt-free. Also, share your thoughts, tips, and ask away any questions in the comment section below!

Good tips on paying debt but for me, I would rather avoid going into debt in the first place. Thanks for sharing.

Thanks John. Yes, avoid getting into debt as much as possible!

This is a really great post! Lots of helpful tips to get rid of debt. Thanks!

Thanks Petra!

Great tips for how to pay off debt! You definitely need to have a plan for paying off debt, whether you have a little or a lot. Having a roadmap to follow can make such a difference in how easily you’re able to make progress.

Thanks Rebecca. Planning and execution is key!

You’ve got some great advice. Ultimately, at the end of the day, the best thing that we can do for our finances is simply to take control and be intentional about them rather than just rolling with whatever situation we’re currently in and letting it happen.

Thanks Britt. 100% agree about taking control!

Very good tips. I find using debit cards also helps. Earmarking is what I did not know before.

Thanks Nadia!

Lots of great tips. Loved the “personal notes”. Thank you for sharing

Thanks Lisa!

Pingback: How to use credit card wisely: Pros and Cons of using a credit card

Great tips. It’s best to get the debts off your head, as early as possible. After all, having a debt is like a burden on head. I appreciate these advices

Thanks!

Great ideas for a complicated problem that many people face. Thanks for sharing!

Thanks Andrea!

Pingback: How To Invest Money - Make Your Money Work For You

Pingback: What Is A Zero-Based Budget - A Step-By-Step Guide For Your Budget

Great tips for paying off debt. It seems like a daunting task, ,but it just takes some dedication and patience.

Absolutely Patricia! It takes time to be financially independent and the more consistent you are, the quicker the results. Thanks!

Awesome tips!! I’ve written some personal finance articles as well if you want to check them out 🙂 https://alliesfashionalley.com/category/money/

Thanks Allie. I will check it out!

great tips and very cool spreadsheet! I use one very similar to keep track of my monthly expenses as well 🙂

Thanks Lucy ????

Great tips. I definitely agree on having a plan and knowing your current expenses as to create a budget. Using a template is a great way to track your progress. Thanks for sharing.

Thanks Angie!

Thanks Angie

Awesome tips! I graduated college last year with debt and I’m trying to find the most reasonable and quickest way to pay it off so its not hanging over my head forever.

Yes make that a priority so you are debt free. Thanks!

Great tips! Getting started towards paying off debts is hard, but in the end, it feels good! My #1 thing was to cut down on takeout/coffees!

Pingback: 10 Best & Smart Investing Strategies For Millennials